Home buyers with mortgages face 28% hit to buying power over 2023 as borrowing costs rise

- Housing market is slowly transitioning to a buyers market as higher mortgage rates set to hit household buying power by up to 28% and asking price reductions return to pre-pandemic levels

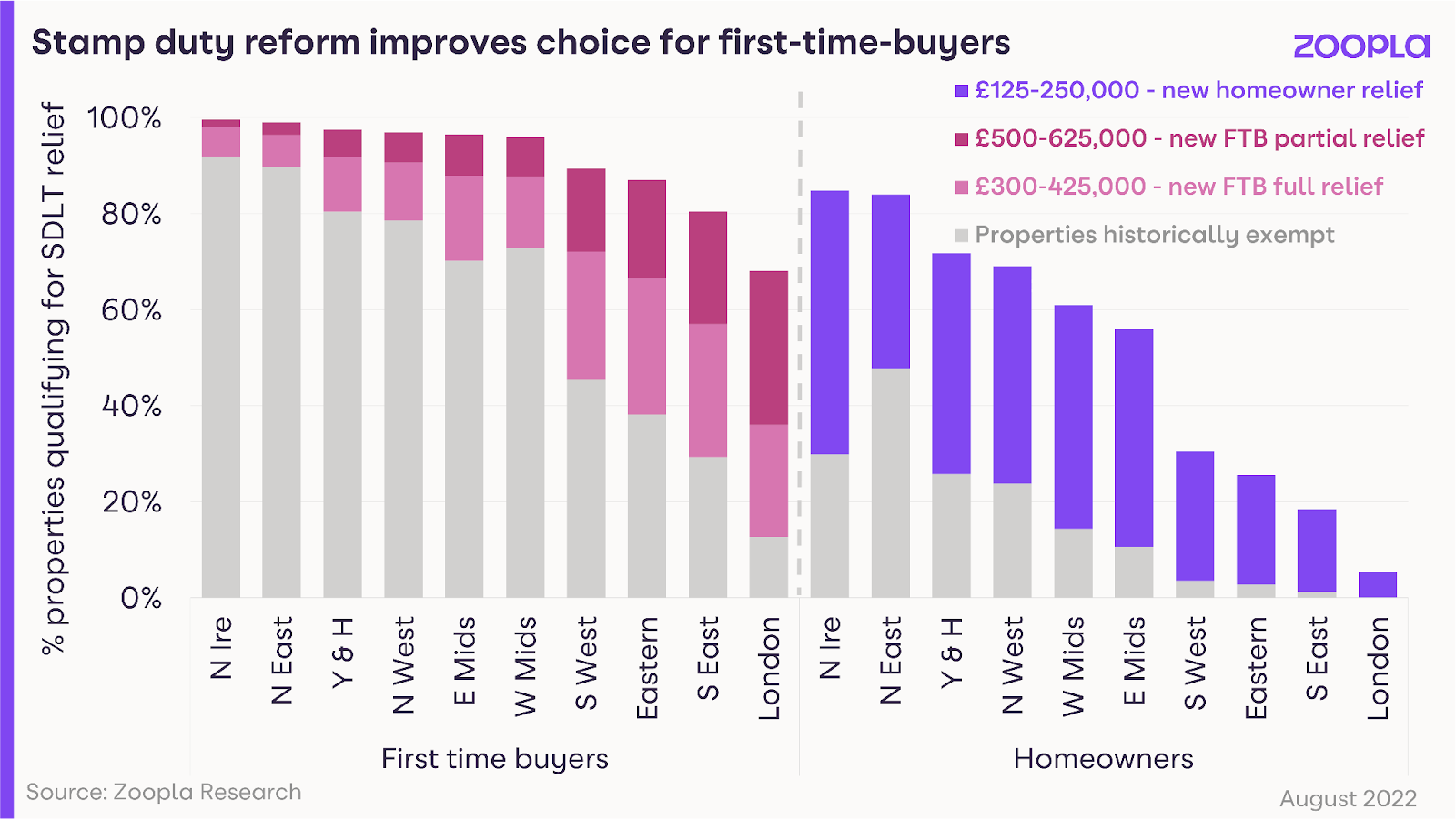

- Stamp duty changes will support lower value markets and help first-time buyers in southern England, while the increase in the stamp duty threshold to £250,000 takes 43% of homes out of stamp duty

- UK house growth remains stable at +8.2% YoY despite increasing cost of living pressures with the pandemic price gains compounding the issue of affordability, especially in southern England

- Some regions including Wales, the North East and Scotland have seen 10 years of growth compressed into just two over the pandemic

PRESS RELEASE: Rising mortgage rates impact buying power – although this will be partially offset by the cut to stamp duty

Despite housing market activity holding up over the summer – the recent spike in mortgage rates for new borrowers is the most important factor for the housing market this autumn. Higher mortgage rates are reducing buying power which could be as much as 28% if mortgage rates reach 5% by the end of the year, assuming buyers want to keep their monthly repayments unchanged.

To offset the hit to buying power, we believe that buyers have three options. They can put down a larger deposit, allocate more of their income to mortgage costs, or adjust their budgets and consider buying a smaller property or purchasing in a cheaper area. We anticipate that higher mortgage rates will have the greatest impact on buying power in high-value markets in London and the South East – as well as regions such as Wales that have registered the greatest surge in house prices over the pandemic.

Stamp duty changes announced last year will support activity in lower value markets and help first-time buyers in southern England, while the increase in the stamp duty threshold to £250,000 takes 43% of homes out of stamp duty and will boost regional markets. The position for first time buyers facing large stamp duty bills improves significantly in southern regions.

Asking price reductions return to pre-pandemic levels

There are early signs that price sensitivity is emerging as 6% of homes listed for sale have seen the asking price adjusted downwards by 5% or more, the highest level since before the pandemic. Re-pricing is a seasonal trend as we enter autumn, however, given the economic backdrop and factors including rising energy prices and rising interest rates – we believe this is a clear sign of a return to more of a buyers market after 2 years of a red-hot sellers market. For sellers, this means there is more of an impetus to shift their mindset when it comes to asking price, and consider local market dynamics more closely as well as the potential types of buyer for their property in the local area.

However, these price adjustments are to be expected as the market shifts from conditions where demand greatly exceeds supply. We do not believe that this is a pre-cursor for big price falls but an indication that the rate of price growth will start to slow more rapidly in Q4 and into 2023 as buyers react to the rising cost of borrowing.

10 years of house price growth compressed into 2 years due to the pandemic

Houses in Wales recorded a 27% jump in prices over the pandemic which is the equivalent to 10 years of pre-pandemic growth compressed into just over 2 years, while a similar pattern has been seen in the North East and Scotland largely due to below-average price growth since 2009.

Whilst London has lagged the rest of the market in terms of annual growth rates, the average house value in London has increased by over £100,000 since the start of the pandemic.

By contrast, the average value of a flat in London has increased just 2.4%. Flat growth is the weakest market segment in percentage terms in the UK as buyers prioritise space and more working from home and working from home hitting the London market more.

“A surge in home values over the pandemic and the rise of mortgage rates means we face a sizable hit to household buying power over the rest of 2022 and into 2023”

Richard Donnell, Executive Director at Zoopla comments: “Measures of housing market activity have been very resilient over the summer. A surge in home values over the pandemic and the rise of mortgage rates means we face a sizable hit to household buying power over the rest of 2022 and into 2023.

“While the recent changes to stamp duty are welcome, supporting activity in regional markets and the first time buyer market in southern England, the increase in mortgage rates will erode much of the gains. Homeowners that want to sell their home this year need to price realistically and seek the advice of an agent on local market trends.”

Director of Benham and Reeves, Marc von Grundherr, commented: “Higher mortgage rates are just one factor contributing to the cost of living crisis, but they’re certainly the most influential factor when it comes to the purchasing power of the nation’s homebuyers. The market is now at a bit of a tipping point where house prices have continued to increase rapidly, but the reality for many buyers is that they are no longer able to stretch themselves financially. This should be an important consideration for those looking to sell and a consideration that must be made when setting your asking price.

“Entering the market with over ambitious asking price expectations is likely to see a property languish with little to no attention from prospective buyers. Even sellers with a more sensible approach may still find that they have to reduce a tad in order to get a sale over the line. The very best course of action in any market is to price appropriately and a good local agent will give you the best idea of current market values in your area, as well as the appetite for your home once it has hit the market.

“Selling at the top end of this valuation will leave you some wiggle room to negotiate downwards to a price you are still happy with and to a price point that will ultimately get you sold. Yes, the latest stamp duty cuts will leave buyers a little extra in their back pocket when it comes to negotiating, but don’t be fooled into thinking this marginal saving will spur them into paying way over the odds for your home. It won’t.”

Business Insider identifies 21 leading Proptechs that can stay the course amid the economic downturn

After a proptech investment boom in 2021, attracting a record-high $32 billion in funding, interest rates are on a perilous upward trajectory. Borrowing remains high and housing markets across the world are slowing, impacting the market for investors and businesses alike.

After a number of high-profile layoffs at top proptech companies, Business Insider polled 12 venture capitalists, who have put forward a list of 21 proptech companies that can weather the current economic climate.

Among them are providers of management software, AI-driven investor platforms, sustainable home builders and much more.

Included in the top 21 most promising proptech companies:

Proptech and Property News in association with Estate Agent Networking.

Andrew Stanton is the founder and CEO of Proptech-PR, a consultancy for Founders of Proptechs looking to grow and exit, using his influence from decades of industry experience. Separately he is a consultant to some of the biggest names in global real estate, advising on sales and acquisitions, market positioning, and operations. He is also the founder and editor of Proptech-X Proptech & Property News, where his insights, connections and detailed analysis and commentary on proptech and real estate are second to none.

-

Andrew Stantonhttps://proptech-x.com/author/andrew-stanton/

-

Andrew Stantonhttps://proptech-x.com/author/andrew-stanton/

-

Andrew Stantonhttps://proptech-x.com/author/andrew-stanton/

-

Andrew Stantonhttps://proptech-x.com/author/andrew-stanton/